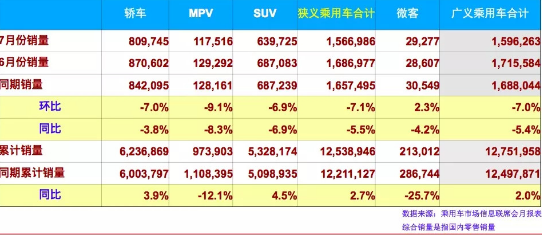

35392 and 26042, these two figures are respectively the number one models in China's sedan and SUV sales rankings in July 2018. Of course, this seems a bit weird, because the SUV camp represented by Great Wall Motors Haval H6 in the past two years, the top few have maintained their sales of several mainstream foreign brand models (Lavi, Corolla, Sylphy, Yinglang) The absolute crush. If I remember correctly, Haval H6 once sold more than 80,000 units in a single month. This is a number that shocks all "countries on wheels" across the ocean. Because there, only Ford and GM pickup trucks can be so "crazy." However, there is no permanent feast in the world. In the Chinese auto market, there is no market segment that can maintain rapid growth for a long time. What is even more worrying is that in July this year, the Chinese auto market saw a single month sales decline of more than 5% year-on-year, which was rare in the past ten years. The most important reason is that the SUV, which is a sales "engine", loses power. Therefore, from the financial reports of listed car companies for the whole year of 2017 and the first half of 2018, it is not difficult to find that companies that rely heavily on SUV products for profit have encountered larger problems and more severe challenges. Dreams will always wake up, but sooner or later. For more than ten years, the growth rate of the SUV market has been like a "spring dream". High premiums, high sales, and high profits have made auto companies feel swayed. Some entered early and made a fortune; some entered late, but still Able to get a share of the increment. But when the growth rate plummeted, what was left to the market was a sorrow, and the contention for increments became a battle for stock. Who was more nervous? "Flaws" of Chinese Brands According to data released by the China Association of Automobile Manufacturers, in July this year, Chinese brand SUV sales were 366,000 units, a year-on-year decrease of 7%, accounting for 57.9% of total SUV sales; from January to July, Chinese brand SUV sales were 335.7 10,000 vehicles, an increase of 8.5% year-on-year, accounting for 60% of total sales, an increase of 0.7% year-on-year. It seems that the share of Chinese independent brands is still increasing. But behind this set of data are the weaknesses that Chinese auto brands have gradually revealed. It also highlights the huge impact of SUV ebbs on some autonomous car companies, and some corporate profit cows are at risk of "weaning". From the data analysis, in July of this year, there were only 4 seats left in the SUV sales list for models that can truly be called independent brands, but the number was doubled in the previous two years. In particular, the top three on the list were occupied by Great Wall, Guangzhou Automobile and Baojun for some time, but the current situation is not optimistic. At present, in the first camp of Chinese auto brands, the ebb of SUV has a greater impact on the two companies, Changan Automobile and Great Wall Motor. Among them, Changan Automobile's three main SUV products did not exceed the 100,000 mark in the first 7 months, which will have a greater impact on its annual performance; although Great Wall Motors still has H6 to support the overall situation, its small SUVs are still emerging fluctuation. However, it is gratifying that Changan Automobile is strengthening its intelligent network connection and model design; in terms of Great Wall Motors, the Haval brand has re-adjusted its product line from red label to blue label to H series and F series. In contrast, Geely, which relies on SUVs and cars to walk on two legs, is more optimistic. Sales of its SUV models are relatively stable. Geely released an announcement showing that in the first half of this year, its sales volume was 766,000 (SUVs accounted for more than 50%), and its net profit reached 6.67 billion yuan, a year-on-year increase of 54%, which was higher than the growth rate of sales and showed high value. The sales momentum of its SUV models is good. However, life is not so easy for the second and third camps of independent brands. Since the beginning of this year, although SAIC Roewe and GAC Trumpchi can maintain growth, the terminal sales pressure is very high. The two "star SUVs", RX5 and GS4, are also facing the challenge of declining sales. From the perspective of Changan, SAIC and GAC's own brands, the weaknesses of these companies are mainly due to the serious "paying on their own money" after the launch of their main models. This is also true in the mid-to-high-end SUV field, which is full of flaws over time. As the third echelon, several major state-owned automobile groups and local state-owned automobile companies, as well as some private companies, face a more severe environment. Companies such as Haima, Dongfeng Fengshen, Jianghuai, etc., due to the low tide of SUVs, on the one hand, these companies introduced low-priced products to temporarily seize the market through the elimination of foreign models or technologies of joint ventures. On the other hand, due to endless product quality problems, lack of core competitiveness, and low brand influence and reputation, consumers are gradually turning away from these brands. Therefore, although the sales of self-owned brand SUVs are still growing, they are showing the "Matthew effect". This situation is especially obvious when the SUV is ebb, and the same is true for foreign brands. The "trouble" of foreign brands In 2018, Volkswagen released its ambitious “Volkswagen SUV Strategyâ€. Even if the SUV trend is low, Volkswagen plans to launch 10 SUV products, in order to achieve the same market share of SUVs and cars; Toyota also launched under the TNGA framework. Two small SUVs are introduced, and it is more direct to seize the entry-level SUV market. According to the plans of these two world auto giants, although they have not caught up with the "first class of high-speed rail" of SUVs, they will never miss the market battle of hard power. It seems late, but as Feng Sihan, the head of Volkswagen's Chinese brand, said, Chinese brands have matured this market, but the more they are, the more they will have latecomer advantages for latecomers with stronger products and brand power. But it is not without trouble for these joint venture companies at the head. With the rise of Geely’s Lynk & Co brand and Great Wall Motor’s WEY brand gaining a foothold, the joint venture’s SUV models are not still superior. Even high-end brands such as Volkswagen, Toyota, and even Audi may be “seeking trouble†by Chinese auto brands at any time. ". In fact, the car K-line believes that, at some levels, the ebb of SUVs will have a greater impact on the joint venture. Because this will cause companies with stronger independent brands to continue to make breakthroughs, and at the same time, luxury brands will also be pressured downward because the market becomes colder. Therefore, foreign brands such as Hyundai Kia and PSA Peugeot Citroen have to lose the face of foreign brands. At the end of last year, in order to increase sales, Hyundai Motor launched the ix35 with a price of 110,000 yuan. This car was once the most important SUV model of Beijing Hyundai in the Chinese market. As a brother of Hyundai, Kia directly pulled the SUV product line of the joint venture to 60,000 yuan, which is directly equivalent to "fighting" with the low-end Baojun brand. Similarly, French cars are not having a good life. The two major brands of Dongfeng Peugeot Citroen have to take price reduction measures as soon as almost new products are launched. Mainstream Chinese brands such as Haval's new H6 and Geely Boyue have eroded its market. Data show that in July, Hyundai Motor's SUV sales fell across the board. What is embarrassing is that ENCINO, which went on sale on April 10 this year and was highly expected by Beijing Hyundai, has sold nearly 4,400 units in the first month of its listing, and has since fallen sharply. Only in July 65 vehicles were sold. This is just a microcosm of the start of Beijing Hyundai in the second half of the year, and it is also a challenge that some joint venture companies may face. The author believes that it is difficult to determine whether the impact on Chinese brands or foreign brands will be greater during this period of ebb in the SUV market. At present, for most auto brands, what they need to do is not only worry about the "ebb" of market demand, but also the "ebb" of product quality, service and confidence. Some analysts pointed out that perhaps this phased decline is temporary, but now it has triggered tensions among major auto companies. GALOCE weight indicators are available in a variety of materials ranging from aluminum to 304 stainless steel enclosures and come with a variety of display options ranging from LCD, LED to large displays and wireless options. output RS232/RS485, can conntact the computer. Optional wall mount kit, stainless steel bracket. Weight Indicator,Digital Load Cell Indicator,Indicator Load Cell, load cell display GALOCE (XI'AN) M&C TECHNOLOGY CO., LTD. , https://www.galoce-meas.com