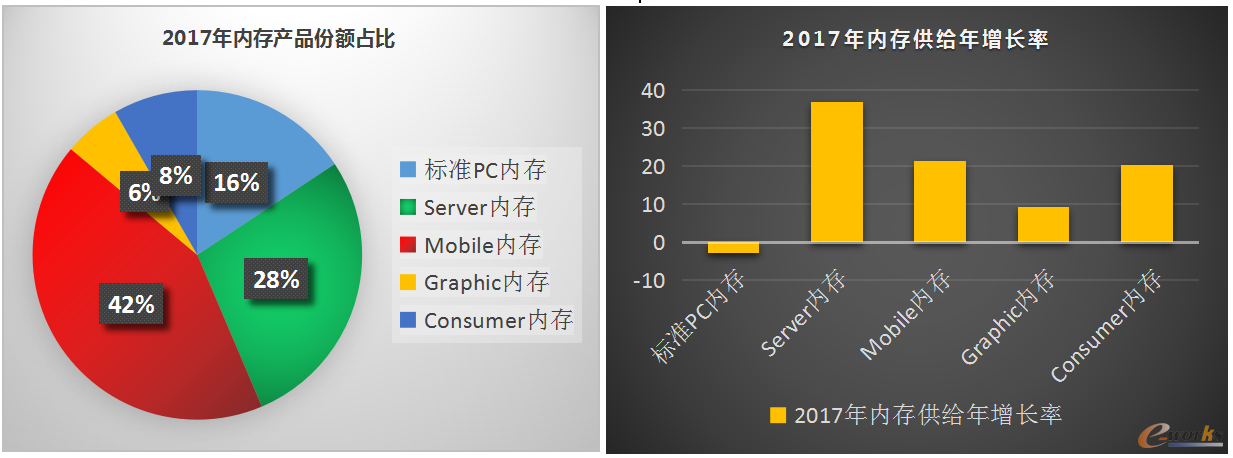

From 2016, soaring storage prices are eroding the profits of the entire machine manufacturer. Whether it is DRAM or NANDFLASH, more than a year is the time, the price is at a record high in almost every quarter. Take Kingston's okko 8GBDDR42400 memory as an example. In November 2016, the price was only 339 yuan. After only one year, the price rose to 969 yuan. It is estimated that such price increases will continue into the first quarter of 2018. With this surge in memory prices, Samsung Electronics has become the company with the highest operating profit worldwide in 2017. Operating profit in the fourth quarter is expected to exceed approximately RMB 60 billion for the first time, an increase of 179% year-on-year; South Korea's Hynix in the third quarter The basic profit reached approximately RMB 21.81 billion, a year-on-year increase of 415%. The United States Micron Technology’s revenue for the fourth quarter was US$ 6.14 billion, which was 91% higher than the same period of last year and exceeds Wall Street’s US$5.99 billion forecast. At a time when the majority of machine manufacturers were suffering from price increases, memory manufacturers ushered in a rare spring. Market: Supply exceeds demand is the root cause of memory prices When it comes to memory prices, some people think that it is caused by a giant monopoly, and some people think that it is a dealer who maliciously picks up goods. However, I believe that the memory production speed can not meet the new market demand is the real reason to promote the continued rise in memory prices. Reviewing the development of the storage industry, ten years ago, memory was mainly used on PCs and servers. However, as the sales volume of these two markets grew steadily, manufacturers can maintain a balance between supply and demand by predicting the market, making memory prices stable. Even with the advancement of technology there will be a decline. Therefore, for a long time, it has always played the role of the "Bcharca Party" in the list of purchases of PCs and server devices. However, in recent years, as new technologies such as mobile terminals, cloud computing, artificial intelligence, Internet of Things, and big data have gradually matured, a large number of applications have begun to land, causing many new product purchase requirements in the market. Users demand faster, higher performance memory products such as solid state drives, flash memory, and more. Statistics show that in 2016 alone, China’s smartphone production reached 1.5 billion units, and 64G and 128G memory have become standard. At the same time, the deployment of large-scale cloud platforms and next-generation data centers has further driven the demand for high-performance memory products. In the PC market, more and more people expect to replace HDDs with SSDs to improve overall performance. According to ICInsights' forecast, the global DRAM market will grow 75% to reach US$72 billion in 2017; the NANDFlash global market will increase by 44% to US$49.8 billion. In 2020, the global market will reach 100 billion U.S. dollars. Source: DRAMeXchange "Global Memory Industry Development Trends 2018" In general, it usually takes 1 to 2 years for a storage plant to go from building to production. If the market changes in the short term and the demand for high-performance memory products is too great, there will be a phenomenon of supply shortage, which will promote the rapid increase in memory prices. Since 2016, memory manufacturers have begun to shift production capacity to new types of flash memory, namely 3D NAND, which has reduced production plans for DRAM and 2D NAND, and the yield of 3D NAND products is very low. As a result, almost all series of storage products are out of stock. Challenge: Rising storage costs erode domestic electronics industry profits At present, China is the world's largest integrated circuit demand market. The data shows that the scale of China's integrated circuit market reached 119.859 billion yuan in 2016, of which the memory market scale was 284.3 billion yuan, accounting for 54.1% of the global share. As the most widely used semiconductor core device, memory is one of the pillar products of integrated circuits. However, the current situation that we have to accept is that China's memory products are still heavily dependent on imports. Currently, in the global semiconductor memory industry, South Korea's Samsung, Hynix, and Micron Technology occupy 93% of the DRAM market, and China’s share is zero; the flash memory market is dominated by Samsung, Hynix, Toshiba, SanDisk, Micron and Intel. Fractions, China's share is still zero; only China Zhaoyi Innovation 2016 in NorFlash chips accounted for 7% of the market. According to statistics, from 2013 to 2016, China's semiconductor memory imports increased by 47.5% in four years, and the amount of imports increased from 46.17 billion US dollars to 68.13 billion US dollars, and it is estimated that it will exceed 70 billion US dollars in 2017. The right to control the semiconductor memory industry is still in the hands of a few foreign companies. The memory price hike has greatly eroded the profits of electronic machine companies and has also affected the development of the industry. Taking the mobile phone industry as an example, Xiaomi and Huawei Technologies, one of the largest mobile phone manufacturers in the country, have seen a significant increase in memory purchase costs since 2016, and their profits have been severely reduced. Faced with the unfavorable situation of memory prices, it is necessary to be able to get the goods, but also to maintain the basic profits, had to increase the price of mobile phones, the result of the price of the cost has been transferred to the consumer body. The memory price increase is even worse for the PC market, which is already sluggish. Many consumers said that due to the high memory prices, they had to temporarily abandon their large memory devices. Some installed shop owners stated that due to memory price increases, computer installed capacity had dropped by 20%, and orders from Internet cafes had dropped by at least 50%. The result of the memory price increase was finally purchased by companies, distributors, and consumers in China's electronics industry chain. Ye Tianchun, director of the Institute of Microelectronics of the Chinese Academy of Sciences, appealed at the international integrated circuit industry development summit forum: “If the Chinese people do not solve the problem of self-manufactured memory chips in the next 30 years, the so-called information age will lose a very important support and basis." Government: Actively guide the development of domestic memory industry Memory is crucial to the development of China's information industry. The development of domestically-produced memory not only satisfies China's huge demand market, and drives the sound development of the entire IC industry chain. It can also completely change the unfavorable situation in which memory is controlled by people. It is also an effective way to catch up with developed countries in the development of the semiconductor industry. The party and state leaders attach great importance to the development of the integrated circuit industry and upgrade it to a national strategic height. General Secretary Xi Jinping instructed him to concentrate his country’s strengths and resources to achieve breakthroughs in the core key technology areas such as integrated circuits, core electronic components, and basic software as soon as possible. Local governments support the storage industry by setting up large-scale investment funds. As of the first half of 2017, the scale of integrated circuit investment funds established by local governments has exceeded 300 billion yuan. Between 2016 and 2017, 10 of the newly established 19 wafer fabs are located in mainland China. In October this year, the National Development and Reform Commission and the Ministry of Industry and Information Technology jointly issued a 2017 major integrated circuit investment plan. The Jinhua DRAM storage project in Fujian was approved to receive 200 million yuan, and the Xiamen Sanan Communications Microelectronic Device Project was approved to be 50 million yuan. The integrated circuit industry investment fund of Anhui Province with a total size of 30 billion yuan was formally established on the 18th. By 2020, Anhui Province plans to build three 12-inch wafer production lines and more than three 8-inch wafer production lines with a combined capacity of over 200,000 tablets/month and an output value of 50 billion yuan. Storage companies are actively deploying their industries, focusing on technological innovation and breakthroughs. Ziguang Guoxin's 60 billion yuan capital will be used for the construction of Flash Memory. Wuhan Xinxin plans to invest US$24 billion to build the domestic IC memory industry base and the first-phase investment of 37 billion yuan in Fujian Jinhua's memory IC production line. project. In addition, in Wuhan, in late March this year, a memory base project with a total investment of approximately 160 billion yuan was formally launched in the East Lake High-tech Zone, and it is planned to achieve a production capacity of 300,000 wafers per month by 2020. Based on this calculation, the total investment in memory chips of the three companies will exceed 255 billion renminbi. At the same time, various storage vendors have made predictions on future capacity, and it will be just around the corner to use domestic memory chips in the next three years. Yangtze River Storage has developed 32-layer, 64-G, 3D NAND chips with independent intellectual property rights in December of this year. The 2018 will achieve mass production, and it is expected to reach a monthly production scale of 300,000 by 2020. Hefei Changxin invested US$7.2 billion to build a 12-inch wafer fab for the development of DRAM products. It is expected to achieve mass production in 2018, and the maximum monthly production will reach 125,000 units. Fujian Jinhua's 12-inch DRAM production line was capped in November of this year. Phase 1 will invest a total of 5.3 billion U.S. dollars. It is expected that the 3rd quarter of 2018 will officially introduce 32-nanometer wafer-based 12-inch wafer production capacity, which is expected to reach 60,000 wafers. . Enterprise: Localization of storage will be a long-term battle Foreign storage giants far surpass Chinese companies in performance and production performance. According to estimates by South Korean experts, the technical capacity of China's memory chips is still 10 to 15 years apart from South Korea. This year, Samsung and Hynix are still expanding their production. In May, Samsung invested 2.7 billion U.S. dollars to increase DRAM production lines in South Korea's Hwaseong Plant. In August, Samsung announced that it will invest 7 billion U.S. dollars in the next three years to expand the largest Xi'an plant in China. NANDFlash production capacity; In November, SK hynix signed a contract with the Wuxi municipal government, planning to invest 8.6 billion US dollars to expand DRAM production capacity. It is estimated that the monthly capacity of the new plant will be 200,000, and the process technology will be locked at 10 nanometers. Memory chips are facing high-tech barriers and fierce global competition. Before that, many manufacturers involved in the field of memory chips were finally forced to withdraw from the market by the “suicide counter-cyclical ruleâ€. Despite having a huge domestic demand market, China's storage industry started late and technology is weak. They want to compete for the market from the Big Three who firmly occupy more than 90% of the market. This is a "war" that is destined to have no smoke and is very difficult. Can imagine. Chinese storage companies should not blindly follow suit and scale up production in light of their own market characteristics. They should combine the characteristics of their own markets, lay out their overall industry development, avoid positive competition and conflicts with foreign competitors, attach importance to new product research and innovation, focus on breakthroughs in key core technology areas, and do a good job at the same time Prepare funds and fight for a protracted battle from scratch to weakness. It is believed that in the next 5 to 10 years, China's storage companies will surely appear as the second "BOE" and create a brilliant industry. I/O Connector,Dvi Connector,Rj11 Connector,Iee1394 Connector Shenzhen Hongyian Electronics Co., Ltd. , https://www.hongyiancon.com